- Category:

Disaster Preparedness -

Last updated:

June 4, 2026

How to Apply for an SBA Disaster Loan

Small businesses are struggling as restrictions are put in place to prevent the spread of the new coronavirus (COVID-19). The government has responded by issuing SBA disaster declarations across the United States and by passing emergency assistance legislation, including the CARES Act, opening up the availability of government small-business loans to help keep businesses open and workers employed.

But it’s vital to understand how these SBA disaster loans work so you know what would be best for your small business. Unfortunately, in the rush to get assistance out the door, the details have not always been communicated clearly. For instance, can an SBA disaster loan be forgiven? Who qualifies under the new law? And how do you apply for different kinds of disaster loans?

Here, we’ll go through what an SBA disaster loan is and some of those important dates, rules and restrictions, as well as some other options offered by states and in the private sector.

What is an SBA disaster loan?

An SBA disaster loan is a low-interest loan offered by the U.S. Small Business Administration to help businesses and individuals to recover from officially declared disasters. Historically, disasters have been declared for catastrophic events like hurricanes, earthquakes and floods, and are limited to a state or territory. Presently, small-business owners in all U.S. states and territories qualify for SBA relief programs related to the coronavirus (COVID-19) pandemic.

Paycheck Protection Program (PPP)

The Paycheck Protection Program (PPP), established in the CARES Act, is essentially a new and temporary SBA relief program. These government small-business loans are meant to incentivize small businesses to keep workers on their payrolls by covering two months of payroll costs (up to $100,000 per employee) plus 25%, up to $10 million.

And PPP loans can be forgiven, provided the funds are used for payroll costs (at least 75%), utilities, rent and interest on mortgages. Full forgiveness is also contingent upon maintaining employment head count and salaries/wages comparable to levels before the coronavirus crisis.

Payments on PPP loans can be deferred for six months and up to a year. Loan terms (for funds not forgiven) range from 1% over 2 years to a max of 4% over 10 years. No collateral is needed. Small businesses and sole proprietors can apply beginning April 3, 2020. Independent contractors and the self-employed can apply starting April 10. The Paycheck Protection Program will be available through June 30, 2020. Monthly payroll figures are calculated as your business’s average monthly payroll over the year prior to the loan’s start date.

Economic Injury Disaster Loans (EIDLs) for COVID-19

Recent congressional action in response to the COVID-19 outbreak has also brought changes to existing government small-business loans by expanding access to SBA Economic Injury Disaster Loans. EIDLs are available to all small-business owners in the United States and U.S. territories.

This SBA relief program provides up to $2 million in assistance. Collateral is required, but a personal guarantee is waived on loans less than $200,000 (before December 31, 2020), and payment can be deferred for up to 12 months.

Economic Injury Disaster Loans can’t be forgiven, but the money can be used more broadly. And some of the funds from an EIDL can be converted to the Paycheck Protection Program to get the benefit of forgiveness for money applied toward payroll. Small businesses are being offered an interest rate of 3.75%, with nonprofits afforded a 2.75% interest rate. How long you have to pay back this SBA loan depends on your needs, but long-term loans are available, up to 30 years.

Can you get an advance on an Economic Injury Disaster Loan?

In an attempt to get badly needed funds to struggling businesses, the SBA is making advances to EIDL applicants of up to $10,000. You can expect to receive the money within three days of a successful application, and the loan advance doesn’t have to be repaid.

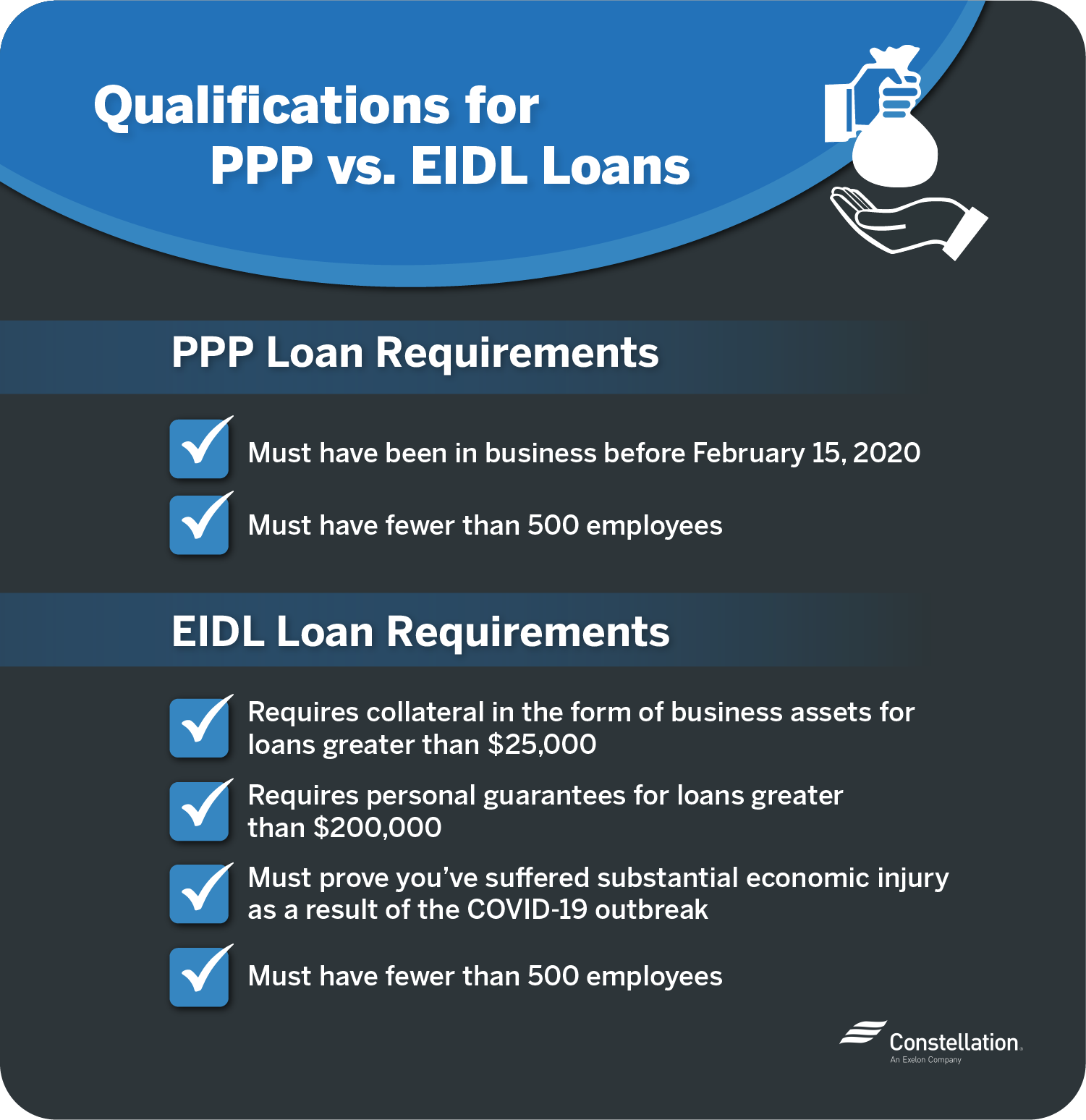

Who qualifies for SBA disaster loans: PPP vs. EIDL

Who qualifies for SBA disaster loans varies slightly between the Paycheck Protection Program and the Economic Injury Disaster Loan Program. Normally limited to the state or territory where the SBA disaster declaration was made, for COVID-19 the declaration was made nationwide.

It’s easier to qualify for PPP because no collateral is required and you only need to have been in business before February 15, 2020. The main SBA disaster loan requirement for PPP is that businesses must have fewer than 500 employees. Applicable businesses include:

- Sole Proprietorships

- Independent contractors

- Self-employed workers

- 501(c)(3) nonprofits

- 501(c)(19) veterans organizations

- Tribal businesses

- Small businesses in hospitality and food service with multiple locations (franchisors and franchisees)

- Businesses in certain industries with more than 500 employees but meet the SBA’s employee-based size standards

Economic Injury Disaster Loans are harder to obtain, requiring collateral in the form of business assets for loans greater than $25,000 and personal guarantees for loans greater than $200,000. You must prove you’ve suffered substantial economic injury as a result of the COVID-19 outbreak. Approval can be based on a good credit score, and your tax records will be subject to review by the SBA. As with PPP loans, there’s a 500-employee cap on business size. Small businesses that qualify include:

- Sole Proprietorships

- Independent contractors

- Employee Stock Ownership Plans (ESOPs)

- Private nonprofits

- Tribal businesses

- Small agricultural/producer cooperatives, aquaculture enterprises and nurseries

- Businesses in certain industries with more than 500 employees but meet the SBA’s size standards

How do SBA disaster loans work?

SBA disaster loans are a means of getting assistance to people whose businesses or homes have been harmed by catastrophic large-scale events, such as the current pandemic. These relief programs become available after SBA disaster declarations are made officially for a state or territory. The terms are set by each borrower’s ability to pay, with the ability to spread out affordable payments over a long period of time.

Although forgiveness sometimes comes into play under specific circumstances, disaster loans distributed by the SBA should not be considered grants. Even with expanded access to EIDLs, applicants must still qualify for loans because they are expected to be repaid. Failure to make payments (that are not deferred as part of the program’s structure) will result in default on your SBA loan.

What can they be used for?

Paycheck Protection Program loans are primarily meant to cover payroll costs, encouraging job retention, whereas Economic Injury Disaster Loans can be used more broadly for operating expenses.

Permitted usage for PPP loans:

- Payroll and benefits

- Utilities

- Rent

- Mortgage interest

Permitted usage for EIDL loans:

- Payroll

- Paid sick leave associated with COVID-19

- Cost increases as a result of the pandemic’s economic disruption

- Rent or mortgage

- Any obligations that can’t be met because of the economic impact of the crisis

It’s important to note that you can’t apply for more than one PPP loan or EIDL. You can get one of each, but they must be used for different purposes. A portion of your Economic Injury Disaster Loan can be converted to a Paycheck Protection Program loan to gain the benefit of forgiveness for funds applied to payroll. However, if you already received a forgivable advance on your EIDL, that will be deducted from the amount forgiven in your PPP loan.

Pros and cons of SBA disaster loans

As the scale of the economic damage caused by the coronavirus pandemic unfolds, there is increased urgency to secure needed funding. Still, there are SBA disaster loan pros and cons to be considered before you make your decision.

Pros of SBA disaster loans

- Favorable interest rates. EIDLs offer 3.75% to small-business owners and 2.75% to nonprofits. PPP loans can be as low as 1%.

- Longer loan terms. Paycheck Protection Program loans can extend 10 years, with Economic Injury Disaster Loans pushing out 30 years.

- Payment deferral. You can defer payments for PPP for six to 12 months and for EIDL for a full year.

- Looser requirements to qualify. An EIDL can be obtained with a good credit score, and PPP requires no collateral at all.

- Limited forgiveness. The EIDL advance of up to $10,000 and PPP funds, if used correctly, can be forgiven.

Cons of SBA disaster loans

- Lengthy approval process. Although the SBA will be working hard to process applications, there’s a lot of bureaucracy to wade through and a multitude of small-business owners looking for help.

- Scrutiny of your business’s finances. The SBA will want to review your tax records if you apply for an EIDL.

- Possible default. Like any loan, there’s the possibility of SBA disaster loan default, resulting in damaged credit, lost collateral and sometimes garnished wages.

Applying for your SBA disaster loan

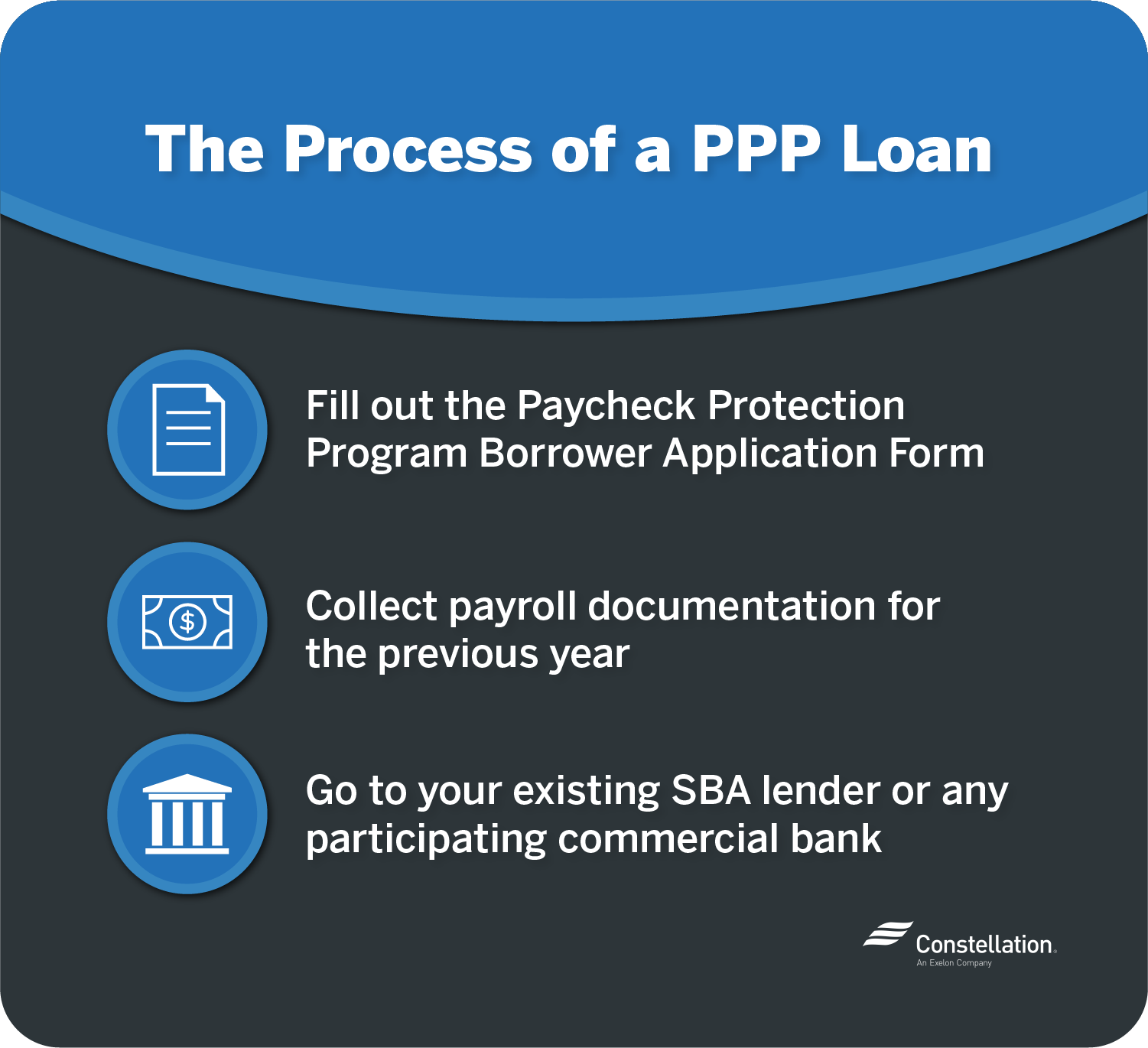

The Paycheck Protection Program doesn’t require applicants to prove economic injury or provide collateral. To apply for a PPP loan:

- Fill out the Paycheck Protection Program Borrower Application Form

- Collect payroll documentation for the previous year

- Go to your existing SBA lender or any federally insured depository institution, federally insured credit union or Farm Credit System institution

The timeline for processing a PPP loan application has yet to be firmly established, but the program is set to expire after June 30, 2020.

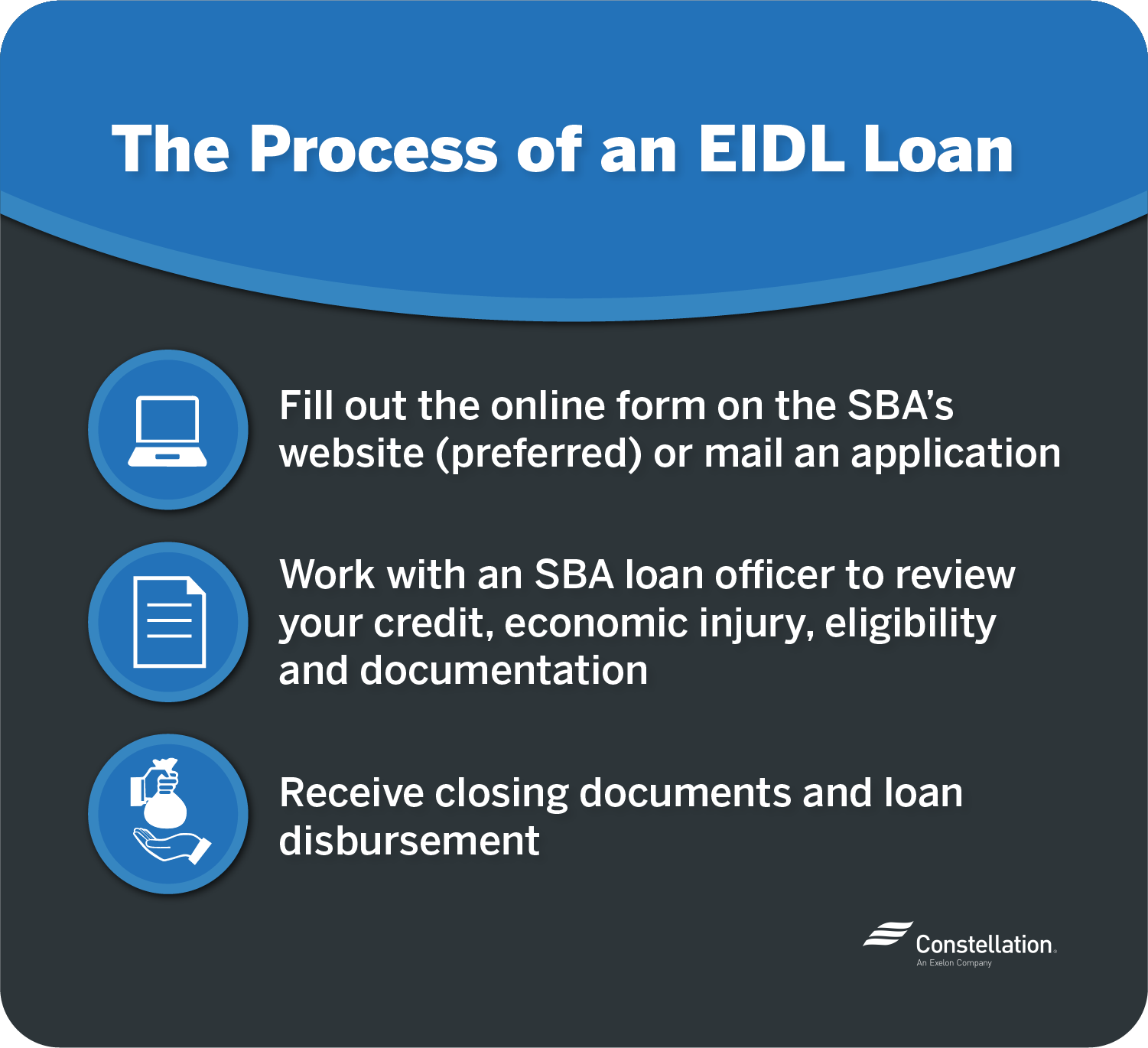

Economic Injury Disaster Loans have more extensive SBA disaster loan requirements. To apply for an EIDL:

- Fill out the online form on the SBA’s website (preferred) or mail an application

- Work with an SBA loan officer to review your credit, economic injury, eligibility and documentation

- Receive closing documents and loan disbursement

The whole process, from beginning to end, could take weeks to months. After the SBA receives your signed closing documents, you should receive your first loan disbursement within five days.

Application requirements for disaster loans

Paycheck Protection Program loans require the previous year’s payroll documentation and the application form. Economic Injury Disaster Loans require the following forms and documentation:

- SBA Form 5. Enter “Economic Injury” as the type.

- Form 4506-T. This allows the SBA to confirm your tax information with the IRS. You’ll need one for the business and one for you.

- Business & personal tax returns. Collect three years’ worth, ideally.

- 2019 income statement. You’ll need to show your business’s performance for each month as well as the year’s total.

- 2019 balance sheet. This sheds light on your asset situation.

- Business debt schedule. You’ll need to provide details about your company’s debt.

- Personal financial statement. Business owners need to list assets, debts and net worth.

(Before applying, you may want to check your personal credit score, as it may affect the success of your application for an EIDL.)

How long do you have to pay back an SBA loan?

Terms are longer for Economic Injury Disaster Loans than for Paycheck Protection Program loans. PPP loans range from two to 10 years, while EIDLs can extend 30 years.

What if your loan defaults?

Economic Injury Disaster Loans require collateral in the form of liens on business assets for loans over $25,000 and personal guarantees for loans over $200,000. If your SBA disaster loan defaults, you stand to lose business or personal assets. Your credit could be damaged. And you may even be subjected to wage garnishment to collect on your unpaid debt.

Can an SBA disaster loan be forgiven?

Some SBA disaster loans can be forgiven, such as the PPP loans or the $10,000 emergency advance for Economic Injury Disaster Loans. Otherwise, SBA loans require payment just like any other loan.

Other government small-business loans and assistance opportunities

Although the SBA disaster loans offered through the Paycheck Protection Program and the Economic Injury Disaster Loan Program are dominating the press coverage, other assistance is available as well — in the form of other government relief programs as well as funds made available by private industry.

Federal small-business relief programs

The federal government has instituted measures to provide assistance to small businesses other than in the form of government small-business loans. In the CARES Act passed in March 2020, Congress created several tax breaks for struggling business owners, and the IRS pushed back the deadline to file 2019 tax returns.

Income tax filing and payment deadline extension

The IRS has extended the deadline for federal tax return filing from April 15, 2020, to July 15, 2020. This applies to all payments up to $10 million and for estimated tax payments for 2020. The extension doesn’t necessarily extend to state or local taxes, so you’ll need to check if they will also allow more time to file.

Subsidy for existing SBA loans

The CARES Act allocated $17 billion to subsidize loans offered through Section 7(a) of the Small Business Act in addition to the new loan programs like PPP. This subsidy can pay six months of principal, interest and fees on qualifying SBA loans.

Tax breaks for small-business owners under the CARES Act

You may want to talk to your accountant about several tax provisions Congress added to the CARES Act to help struggling businesses find extra cash, including:

- Waiving the usual 10% penalty fee for individuals younger than 59 ½ taking money out of a qualified retirement plan in 2020. It must be a “coronavirus-related distribution” no more than $100,000.

- Delaying payment of employer payroll taxes. The amount due from enactment through December 31, 2020, would be deferred, with 50% due December 31, 2021, and the other 50% due December 31, 2022.

- Reversing changes to net operating loss rules. You’ll be able to carry losses from 2018, 2019 and 2020 back five years, or carry it forward, with 2019 and 2020 losses able to offset 100% of taxable income.

State small-business relief programs

States are also trying to put together their own relief programs. In the wake of the outbreak, coronavirus relief legislation is pending in several state legislatures. Some of the programs initiated to date include:

- California — San Francisco’s COVID-19 Small Business Resiliency Fund and the Los Angeles City Small Business Emergency Microloan Program

- Illinois — Chicago Small Business Resiliency Fund

- New York — New York City’s Employee Retention Grant Program and Small Business Continuity Loan Fund

- Florida — The Florida Small Business Emergency Bridge Loan Program

Private sector small-business relief programs

Some banks, utilities, retail energy providers, and creditors have reached out to customers about possible deferment of payment and waiving some penalties for nonpayment. In addition some corporations have stepped up with small-business coronavirus relief programs of their own.

Amazon Neighborhood Small Business Relief Fund

Amazon is offering grants to neighboring small businesses in the South Lake Union and Regrade neighborhoods of Seattle along with the town of Bellevue, Washington. Qualifying service or retail businesses must have fewer than 50 employees and less than $7 million in annual revenue. This grant is not associated specifically with COVID-19.

Facebook Small Business Grants Program

Facebook is offering a total of $100 million in grants and ad credits to 30,000 small businesses affected by the pandemic, across 30 countries. To qualify for a grant, your business must have two or more employees but less than 50, have been in business for at least a year, be located near a Facebook location and have been adversely affected by the coronavirus outbreak.

Whether you decide to apply for a federal SBA disaster loan or seek assistance locally or privately, the common thread running through all options is time sensitivity. To that end, small-business owners in need of more immediate assistance should consider the forgivable $10,000 advance on an Economic Injury Disaster Loan, which can be processed in days rather than weeks or months.

Regardless, the sooner you start the loan application process, the sooner your business could get the funds it needs to continue operation during this difficult time.